This post first appeared on GAO Reports. Read the original article.

What GAO Found

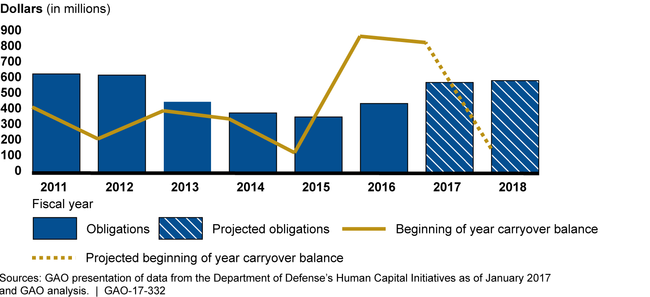

The Department of Defense (DOD), enabled by congressional action, has improved the timeliness of the funding process for the Defense Acquisition Workforce Development Fund (DAWDF). For fiscal year 2015, DOD was authorized to transfer expired funds, which allowed it to fund DAWDF in 2 months. In contrast, for fiscal year 2014, DOD relied on the military departments and other defense agencies (referred to as components) to remit funds to the DOD Comptroller, which took 24 months to complete. As a result, hiring, training, and other initiatives were delayed. Congress also took action in 2016 to reduce the amount of funding carried over from year to year, which totaled $875 million at the beginning of fiscal year 2016, or nearly twice the amount DOD eventually obligated for that year (see figure). GAO estimates that the amount of carryover funds at the beginning of fiscal year 2018 will be reduced to about $156 million.

Defense Acquisition Workforce Development Fund (DAWDF) Funding Carried Over from Year to Year Is Expected to Decrease Significantly by Fiscal Year 2018

In the past year, DOD has taken several actions to improve its management and oversight of DAWDF, including issuing an updated acquisition workforce strategic plan and DAWDF operating guidance. For example, DOD’s August 2016 DAWDF guidance required components to submit annual and 5-year spending plans and formalized the requirement to hold a midyear review to assess DAWDF execution and discuss best practices. However, GAO found that DOD components identified more than $3 billion in potential DAWDF funding requirements for fiscal years 2018 through 2022, which may exceed available funding over this period. Clearly aligning DAWDF funding with DOD’s strategic plan—as GAO recommended in June 2012—may help DOD determine how to prioritize these requirements. GAO also found that components’ guidance, practices, and views on whether they could use DAWDF to pay for personnel to manage the fund varied. Further, GAO found components did not have processes to verify the accuracy and completeness of data reported on DAWDF-funded initiatives. Internal control standards indicate that consistent policies and accurate data can help ensure that funds are used effectively and as intended. Without such controls, DOD could be missing opportunities to use DAWDF more effectively to improve its acquisition workforce.

Why GAO Did This Study

Congress established DAWDF in 2008 to provide DOD with a dedicated source of funding to help recruit and train members of the acquisition workforce. Since 2008, DOD has obligated more than $3.5 billion to meet those objectives. However, in 2012, GAO reported that DOD’s ability to execute hiring and other initiatives had been hindered by delays in the DAWDF funding process, resulting in a large amount of unused funds being carried over from year to year.

GAO was asked to review DOD’s management of DAWDF. This report examines (1) the process DOD uses to fund DAWDF and (2) DOD’s DAWDF management and oversight. GAO analyzed relevant legislation; DOD’s, the military departments’, and other defense agencies’ guidance and processes; and DAWDF budget and initiative execution data. GAO also interviewed DOD officials and conducted a nongeneralizable sample of 10 fiscal year 2015 DAWDF initiatives based on type of initiative and dollar value.

What GAO Recommends

DOD should (1) clarify whether DAWDF funds could be used to pay for personnel to help manage the fund and (2) ensure that DOD components have processes in place to verify the accuracy and completeness of DAWDF data. DOD partially concurred with both recommendations, and has taken or plans to take actions to address them.

For more information, contact Timothy J. DiNapoli at (202) 512-4841 or dinapolit@gao.gov.