This post first appeared on GAO Reports. Read the original article.

What GAO Found

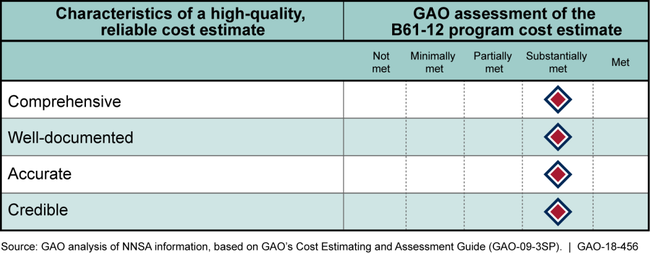

The National Nuclear Security Administration (NNSA) incorporated most cost estimating best practices to develop the program cost estimate for the B61-12 Life Extension Program (LEP), which seeks to consolidate four versions of a nuclear weapon—the B61 bomb—into a bomb called the B61-12. As shown in the figure below, the program substantially met best practices for ensuring the estimate was comprehensive, well-documented, accurate, and credible.

Results of GAO’s Assessment of the B61-12 Life Extension Program Cost Estimate Compared with Best Practices

The B61-12 LEP’s program cost estimate differs from an estimate prepared by another NNSA office independent of the program primarily because the program used different methods and assumptions than the independent office. The program developed its estimate by compiling cost and schedule estimates for activities at each of the NNSA contractor sites participating in the LEP. In contrast, the independent office evaluated program activities completed to date and applied a historical model to estimate costs and durations for remaining activities. NNSA management met with officials from both offices to reconcile the estimates but did not document the rationale for adopting the program estimate unchanged. GAO recommended in a January 2018 report that NNSA document and justify such decisions, in part because GAO’s prior work has shown that independent cost estimates historically are higher than programs’ cost estimates because the team conducting the independent estimate is more objective and less prone to accept optimistic assumptions. In response to the January 2018 report, NNSA agreed to establish a protocol to document management decisions on significant variances between program and independent cost estimates, but it has not yet provided evidence that it has done so.

NNSA and the Department of Defense (DOD) have identified and are managing risks that could complicate efforts to meet the LEP’s fiscal year 2025 completion date. Risks within the program’s areas of responsibility include an aggressive flight test schedule for bomb delivery aircraft. The program is managing these and other risks with a formal risk management process. The program has also taken steps to address risks outside its direct control, such as risks related to the readiness and certification of the weapon’s F-35 delivery aircraft, by providing information to the responsible DOD organizations.

Why GAO Did This Study

Weapons in the U.S. nuclear stockpile are aging. To refurbish or replace nuclear weapons’ aging components, NNSA and DOD undertake LEPs. The B61-12 LEP is the most complex and expensive LEP to date. In October 2016, NNSA formalized a program cost estimate of about $7.6 billion, which is lower than an independent cost estimate of about $10 billion.

Senate Report 113-44 included a provision for GAO to periodically assess the status of the B61-12 LEP. This report assesses (1) the extent to which NNSA followed best practices for cost estimation in producing the program cost estimate for the B61-12 LEP; (2) the reasons for differences between the program cost estimate and the independent cost estimate and how the differences were reconciled; and (3) the extent to which NNSA and DOD have identified and managed program risks. GAO assessed the program cost estimate against best practices, reviewed NNSA and DOD documents, conducted site visits to four NNSA and Air Force sites responsible for design, production, and management activities, and interviewed NNSA and DOD officials.

What GAO Recommends

GAO is making no new recommendations but discusses a prior recommendation that NNSA document and justify decisions regarding independent cost estimates. NNSA provided technical comments, which GAO incorporated as appropriate. DOD did not have any comments.

For more information, contact Allison Bawden at (202) 512-3841 or bawdena@gao.gov.